The Psychology of Hype Cycles

A priest and the dot-com bubble, FOMO and the rational mind, Why we do this every time

The Priest and the Dot-com Bubble

In 2000, at the absolute top of the dot-com bubble, my mentor held a puja at his home in Silicon Valley. A Hindu priest came over and spent two hours doing the full ceremony — Sanskrit chanting, the fire, the marigolds … deeply solemn and properly ancient.

Then, ritual complete, the priest started wandering the house. He scans the bookshelf, then turns around and says:

“I hear there’s a lot of money in networking these days. Could I borrow your Cisco CCNA certification book?”

I think about that priest a lot. Because when the man who came to bless your house against material attachment is eyeing your networking books, the bubble has reached a state of thermodynamic completeness. There is no one left to convert. The mania has saturated every layer of society, right down to the clergy.

And to be fair to the priest, at that moment Cisco was widely expected to become the world’s first trillion-dollar company. The stock peaked a few weeks later, then fell 86% from its March 2000 high and would not return to that price for more than twenty five years.

That’s the thing about manias. Right up until they aren’t, they make complete sense.

When the rest of the world is mad, we must imitate them in some measure

Getting caught in a hype cycle is not a sign that you’re lacking in judgement. It is very nearly the opposite.

In 1720, Isaac Newton, Master of the Royal Mint, co-inventor of calculus, and one of the most powerful minds of his age, got caught in the South Sea Bubble. He owned South Sea stock early, sold during the rise for a handsome profit then watched the mania continue without him. When he was asked whether South Sea stock could keep rising, Newton supposedly said: “I can calculate the motions of the heavenly bodies, but not the madness of people.”

Eventually FOMO got the better of him, he bought back in near the top. When the bubble burst, he lost a fortune.

A London banker captured the psychology even better when he justified subscribing to South Sea stock at its peak: “When the rest of the world is mad, we must imitate them in some measure.”

That is the entire psychology of hype cycles in a few words.

Crypto mania

By the back half of 2020 the crypto craze had gotten very strange. Of course, there was Beeple selling a JPEG for $69 million and Justin Bieber spending $1.3 million on his cartoon ape.

But even around me, smart engineers, level-headed people with mortgages, were routing a slice of every paycheck straight into BTC, ETH and other questionable tokens via direct deposit. Because, and I remember the logic vividly, none of us could construct a future in which Bitcoin did not eventually become an alternate asset to gold. The absence of imagination felt like evidence. If you can’t picture the downside, surely there isn’t one.

Experts like Balaji Srinivasan, former CTO of Coinbase, former a16z general partner, one of the most credentialed minds in tech, were making the rounds on every serious podcast constructing an airtight intellectual case for Bitcoin and wagered that it would hit $1M within 90 days. Well, it didn’t.

But in the moment, none of it felt insane. It felt like being early. The All-In Podcast, four very smart, very rich men with a devoted following, spent episodes earnestly explaining how NFTs would rewire the economics of art collection entirely, handing creators direct relationships with collectors and cutting out the gallery class forever.

FOMO and the rational mind

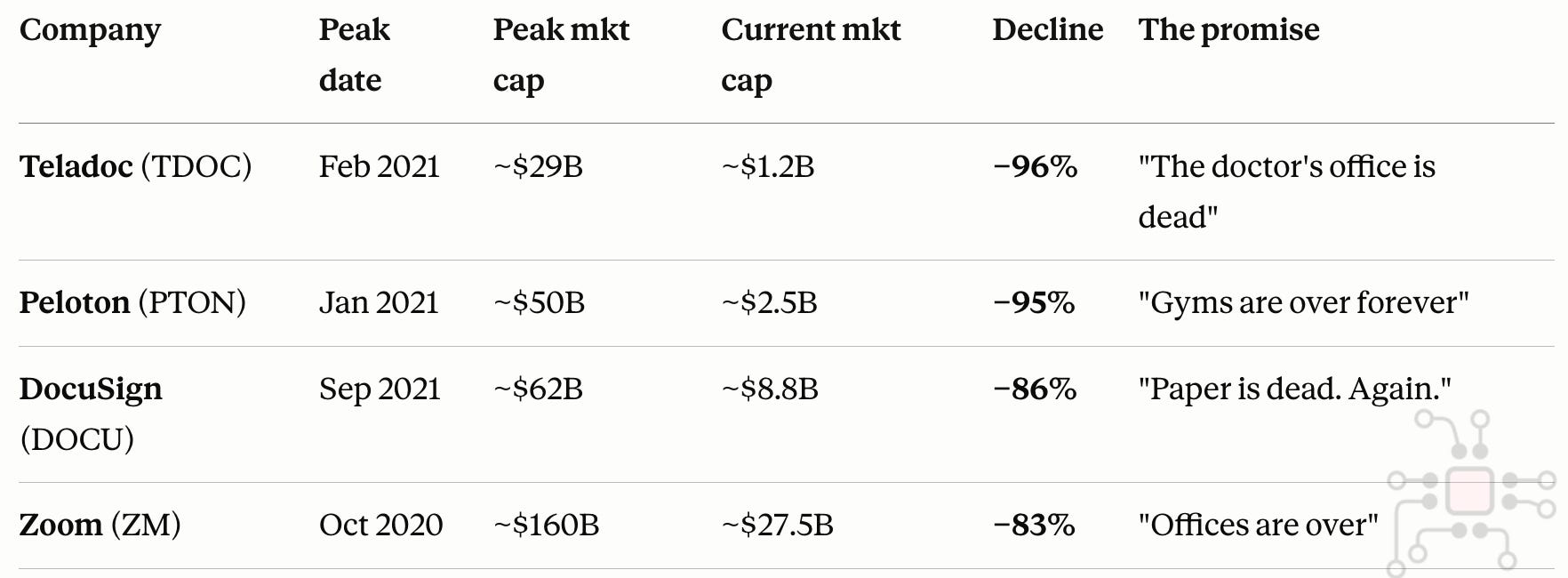

This is the one that still gets me. I knew someone, a disciplined, boring-in-the-best-way boglehead-index investor, the guy who lectures you about expense ratios and time in the market. In late 2021 he abandoned all of it and moved a portion of his money into Cathie Wood's ARK Innovation ETF (ARKK), the flaming emblem of the growth-stock boom, and a few such ETFs (including Peloton, Docusign, et. al). His reasoning was that it’s a new world, work from home is here to stay, it was simply impossible to imagine a future where software lost.

ARKK had closed at $155.30 on February 12, 2021. By late December 2022 it was around $30 — a roughly 80% peak-to-trough collapse.

At DocuSign’s $62 billion peak, I was working at Palo Alto Networks genuinely confused. We were shipping hardware into the networks of every major bank, insurer, and government agency in the world. They had figured out a nicer way to sign a PDF. The market said they were worth more. I still don’t fully understand it.

Why we do this, every time

Strip away the technology and every bubble starts to look the same, because the wiring underneath is the same. Two quotes capture the syndrome better than almost anything else.

“Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, and one by one.”

Charles Mackay, Extraordinary Popular Delusions and the Madness of Crowds (1841)

"There is nothing so disturbing to one's well-being and judgment as to see a friend get rich."

Charles Kindleberger, Manias, Panics, and Crashes: A History of Financial Crises (1978)

Look at the dates on those quotes. Someone once said the lifespan of financial memory is no more than 20 years. Roughly the time it takes for a new generation, always supremely self-confident, to show up convinced they've discovered something the old fools never understood.

As I write this, SpaceX just went public at a ~$1.75 trillion valuation. The largest IPO in history, and Jim Cramer is on television suggesting it could touch $5 trillion by the close. Morningstar's independent estimate of fair value is about $780 billion, less than half the offer price.

Conclusion

I’ll leave you with this.

We always overestimate technology in the short run and underestimate it in the long run. The dot-com mania was an insane bubble and at the same time correct about the internet. The skeptics won the valuation debate. The believers won the technology one.

AI and SpaceX are almost certainly the same shape. The technology is real. The prices being quoted this quarter are, if three centuries of financial history mean anything, probably nonsense. Both things, simultaneously.

The trap was never believing in the technology. The trap is believing you can no longer imagine it going wrong.

Funny style keep doing it

Nicely written, great read.