DRAM was the worst business in chips, now Micron is worth $1 trillion: 6 cycles of boom and bust and what could come next

How the cycle that built and buried memory companies broke, and the mistake Micron can't afford to repeat

On May 26, 2026, Micron closed above a $1 trillion market cap for the first time. The stock went up 19% in a single session after UBS tripled their price target from $535 to $1,625, citing long-term supply agreements with partially fixed pricing. SK Hynix crossed the same threshold the same week.

The headline numbers from Micron’s most recent quarter were quite staggering:

Q2 FY26 revenue of $23.86 billion, up 196% year-over-year and 75% sequentially, with non-GAAP gross margins of 75%.

Q3 guidance: $33.5 billion in a single quarter at roughly 81% gross margin. That’s more than Micron’s entire annual revenue in any year through fiscal 2024.

The company’s entire 2026 HBM output is sold out under multi-year contracts.

To understand how strange this is, you need to know how broken the DRAM business was for the thirty years before this. There’s also a cautionary tale for those who hold $MU.

The Bad Old Days

DRAM was the worst business in semiconductors. Worse than foundry, worse than analog, worse than discretes. The product was a pure commodity, sold by the bit, indistinguishable across vendors. Five or six players were always willing to flood the market the moment demand softened. Every downturn turned into a price war, and every price war took out at least one company.

Toshiba exited in 2001.

Mitsubishi rolled its DRAM into Elpida, which itself went bankrupt in 2012 and got absorbed by Micron.

Powerchip, ProMOS, Nanya spent the 2010s on life support.

The one that hit closest was Qimonda, an Infineon spinoff where a close friend of mine worked as a custom layout engineer. When the 2008 financial crisis hit, DRAM spot prices collapsed — down 85% in 2007 and another 58% in 2008. Samsung, with the deeper balance sheet and the better process node, kept producing flat-out. Qimonda spent 2008 selling every wafer at a loss, racing to shrink to a smaller node before cash ran out. They didn't make it. The company filed for bankruptcy in early 2009. About 12,000 people lost their jobs globally — my friend among them.

This was the routine in DRAM, not a 2008 thing. You worked on a part that competed entirely on price, sold to customers who would switch suppliers for half a cent. The engineering was brilliant, DRAM scaling is some of the hardest physics in the industry, and the financial outcomes were terrible.

I used to drive past a Micron building on Montague Expressway in San Jose every day. Post-2009, the parking lot emptied. Then the sign came down. The intersection sat quiet for years. That building, more than any chart I could draw, is what DRAM economics looked like for the people inside the industry.

Six Cycles of Boom and Bust

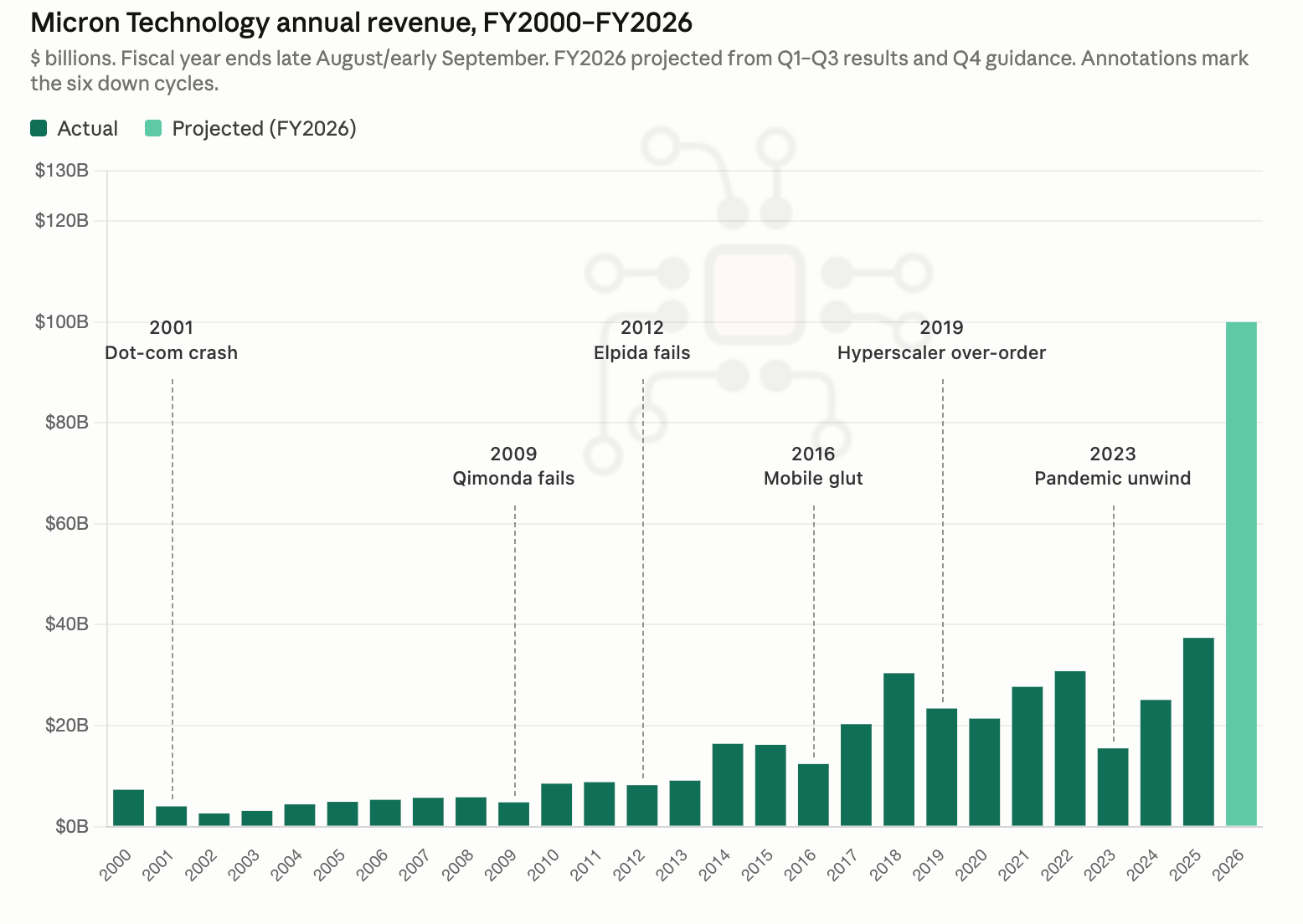

Between 2000 and 2023, the DRAM industry ran through six distinct cycles. Each one a peak followed by a price collapse, and each collapse taking at least one player out of the business or close to it.

2001: Dot-com crash. When the dot-com bubble burst, enterprise IT spending evaporated overnight and PC shipments fell off a cliff. PCs were roughly 80% of DRAM demand at the time, so PC weakness translated directly into a DRAM glut. Micron's revenue went $7.3B → $4.0B → $2.6B over two fiscal years. Every memory maker bled cash. Toshiba quietly exited DRAM in the aftermath.

2008–2009: Financial crisis and Qimonda’s collapse

DRAM prices fell 85% in 2007 and another 58% in 2008 as global demand collapsed and Samsung kept its fabs running flat-out. Qimonda filed insolvency in January 2009. About 12,000 jobs gone worldwide, and one fewer competitor in DRAM forever.

2012: Elpida bankruptcy and the three-supplier era

Elpida was Japan’s last DRAM maker, a 1999 consolidation of the memory divisions of Hitachi, NEC, and Mitsubishi, formed precisely so Japan could keep at least one company in the game.

It didn’t work. Elpida filed bankruptcy in February 2012 and Micron acquired the bones in 2013 for around $2.5 billion. The deal gave Micron mobile DRAM scale and effectively reduced the global DRAM industry from five-plus players to three: Samsung, SK Hynix, and Micron.

The “three-supplier era” matters because three players can coordinate on supply discipline in a way that six cannot. This is the structural change that makes today’s pricing power possible. Without it, the AI surge would have triggered the usual response of everyone over-investing into a glut.

2016: The mobile glut

After the financial crisis, the engine of DRAM growth shifted from PCs to smartphones. Mobile DRAM became the highest-volume product in the industry. But in 2015–2016, smartphone shipments plateaued, (especially in China, which had been the biggest growth market) exactly as memory makers were ramping new mobile DRAM capacity for the demand they thought was still coming.

The result was a familiar inventory glut and price collapse, this time concentrated in mobile DRAM. Micron’s revenue dropped from $16.2B to $12.4B in a single fiscal year. The next leg of growth came from somewhere unexpected: server DRAM for the early cloud buildout, which set up the 2017–2018 super-cycle.

2019: The first hyperscaler over-order

This is key to the current situation.

2018 was a DRAM super-cycle.

Industry revenue hit $99B and Micron did $30.4B at nearly 60% gross margins.

The driver was hyperscaler data-center buildout — AWS, Azure, and Google Cloud all ordering DRAM in volumes the industry had never seen.

Then in early 2019, they stopped. They had massively over-ordered.

Inventory at the hyperscalers ran six to nine months long and they didn’t need to buy new memory for almost a year. DRAM prices fell roughly 60% over four quarters. Micron revenue went $30.4B → $23.4B → $21.4B. Every memory maker took losses. This is the precedent that should keep Micron shareholders honest at $1T. The last time hyperscalers became the dominant buyers, they over-ordered and crashed the cycle within a year.

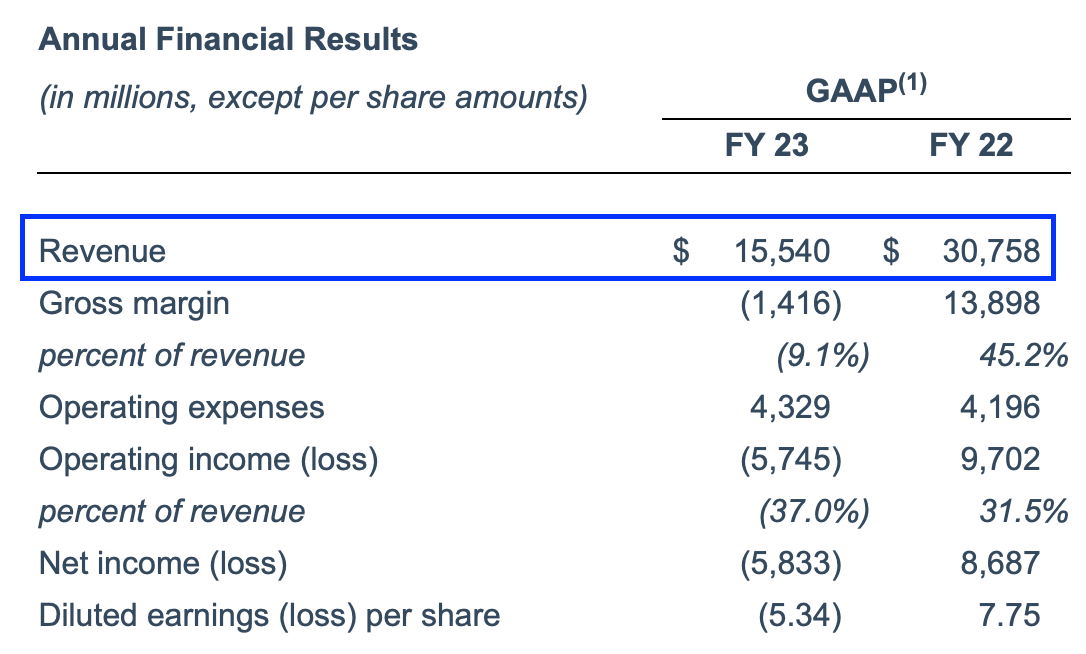

2023: The latest trough

Pandemic-era demand (laptops, gaming consoles, cloud infrastructure during work-from-home) pulled DRAM consumption forward into 2020–2022. When it reversed, it reversed hard.

Micron’s revenue halved from $30.8B in FY2022 to $15.5B in FY2023, and the company lost money every quarter that year. At the time it looked like a normal cycle bottom. Bad, but rhyming with 2009 and 2019.

Micron at $1T: Three Questions That Matter

Whether Micron can justify a $1 trillion valuation depends on three connected questions.

First, engineering: can Micron stay at the frontier of memory technology, especially in HBM, where density, bandwidth, thermals, yield, and packaging all have to improve together?

Second, finance: will the AI capex cycle keep expanding fast enough to absorb the memory capacity now being built?

Third, strategy: are Micron’s customer agreements structured in a way that makes this cycle different from the old DRAM boom-and-bust pattern?

Let’s look at Micron through these three lenses.